The Independent Uganda: You get the Truth we Pay the Price

The Independent Uganda: You get the Truth we Pay the Price

By Joseph Were

Uganda is the easiest place on earth to hire and fire workers, has the most flexible wage policies, is favourable to foreign direct investment and ownership of businesses, and has limited restrictions on capital flows.

But it also has high favouritism amongst government officials, limited public trust in politicians, poor electricity supply, poor internet in schools and poor railway infrastructure.

The result of these indicators is that Uganda is one of the worst places in the world to do business according to the 2009 Global Competitiveness Index (GCI) issued this month by the World Bank in partnership with the African Development Bank and the World Economic Forum.

It assesses economies on how easily one can start a business, get construction permits, employ workers, register property, get credit, protect investment, pay taxes, trade across borders, enforce contracts and close a business.

Competitiveness, according to the report, means productivity. It measures how efficiently firms are able to convert inputs or costs into output, sales or prosperity of a country.

“The more competitive economies tend to be able to produce higher levels of income for their citizens,” the report notes.

This year’s results are particularly important because they come at a time of global financial gloom and yet they show that Uganda’s competitiveness has been declining year-by-year since 2004.

Over the same period, regional neighbours, especially Kenya and Tanzania, have been improving their competiveness and becoming more attractive to businesses.

This year, Uganda is the 6th worst place to do business in the world; placed at number 128 out of the 134 countries surveyed. The worst is Chad followed by Zimbabwe at 133 and Burundi at 132. Kenya is the region’s best at number 93 and Tanzania is at 113. Rwanda was not ranked.

On a scale of zero for worst and seven for best, Uganda scored 3.5 in 2004, 3.4 in 2005 and 2006, and 3.3 in 2007, 2008, and 2009.

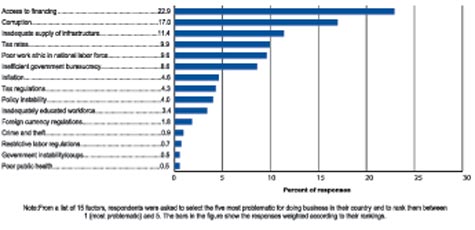

It scores worst on favouritism in decisions by government officials , main telephone lines per 100 people, number of procedures required to start a business, buyer sophistication, and firm-level technology absorption and brain drain.

Globally, both North Africa and sub-Saharan Africa, on average, are outperformed by Southeast Asia. North Africa is ahead of Latin America, and also scores significantly higher than sub-Saharan Africa. Only four countries from the African continent figure in the top half of the overall ranking: Tunisia, South Africa, Botswana, and Mauritius.

Cheap labour

Uganda ranks 25 in labour market efficiency, but is at the second to the bottom in health and primary education.

Gambia (38th) and Kenya (40th) are the two other African countries with the most efficient labor markets in Africa. These three countries are characterized by flexible hiring and firing practices and relatively low non-wage labor costs.

The report notes that African countries are among the least flexible and efficient in the world and that “much must be done on the continent to free Africa’s labor markets and unleash the potential of the region’s workers”.

The report combines the perceptions of leading business executives and compiles data on government and public institutions, infrastructure, innovation and technology, education and human capital, financial environment, domestic competition, company operations and strategy, environment, social responsibility, travel and tourism, and health.

Some of the data is collected through face-to-face interviews with hundreds of entrepreneurs. The responses reflect the managers’ actual experiences. These are then compiled under the 12 pillars of the so-called GCI basic requirements like favourable institutions, infrastructure, macroeconomic stability, health and primary education on a three-stage tier.

A country like Uganda which depends on unskilled labour and natural resources should be perfecting its competiveness based on these basic requirements and also transitioning into the second stage which focuses on improved higher education and training, goods market efficiency, labor market efficiency, financial market sophistication, technological readiness, and market size, which are the so-called efficiency enhancers. The last set of pillars is so-called innovation and sophistication factors which include the level of business sophistication and innovation.

The report also uses the so-called Enabling Trade Index (ETI), to benchmark countries and regions. The ETI measures the factors, policies, and services facilitating the free flow of goods over borders; for example, market access, border administration, transport and communication infrastructure, and business environment.

These are further broken down into tariff and non-tariff barriers, proclivity to trade, efficiency of customs administration, efficiency of import-export procedures, transparency of border administration, availability and quality of transport infrastructure, availability of quality of transport services, availability and use of information and communication technologies (ICTs), regulatory environment, and physical security.

It compares, for example, how costly it is to run a business in Africa compared with other regions in the world. Costs associated with doing business include labor, finance, infrastructure, and the business environment divided into direct, indirect, and invisible costs.

African firms are least competitive because, according to the report, they are almost 20% more expensive to run than firms in East Asia.

Corruption

Secondly, most of the competitive disadvantage of African firms is due to invisible costs””that is, losses experienced by African firms because of the poor infrastructure, demanding credit market, and burdensome regulatory environment, including corruption and lack of security.

Africa also has the worst financing indicators. With the exception of Mauritius and South

Africa, African financial systems are among the smallest in absolute terms and relative to economic activity. Many African financial systems are smaller than a mid-sized bank in continental Europe, with total assets often less than US$1 billion.

Trade

Uganda is favourably ranked on the ETI.

At 79th position globally, it is ranked 4th in the Sub-Saharan Africa region, just behind Namibia.

Uganda’s main comparative strength is its regulatory environment (33rd), with rules encouraging FDI and the ease of hiring foreign labor. Uganda is also characterized by higher levels of market access (58th). Data on non-tariff measures point to a fairly low level of these measures, although Uganda uses high tariffs””in particular on agricultural products””to protect the local producers.

However, in contrast to many other countries in the region, Uganda allows over half of its imports to enter duty-free (58th). This is, to a certain extent, a result of the regional trading agreements concluded with neighboring countries under the East African Community (EAC).

Uganda’s customs administration is somewhat efficient by regional standards (62nd) and compares relatively well with other countries in the region (6th).

Nevertheless, the cost for importing goods remains very high at US$2,900 per container, and some concerns about the burden of customs procedures remain among the business community (85th), although many services have been put in place in the customs administration (50th).

Uganda’s transportation and communications infrastructure is comparatively underdeveloped (93rd) with quality of infrastructure facilities across practically all modes of transport rated as poor.

The availability and usage of Information Communication Technologies, such as fixed and mobile telephones, broadband and Internet is very limited compared with the already low regional standards resulting in Uganda’s 21st rank in the region.

The GCI takes into account the fact that countries around the world are at different levels of economic development.

“What is important for improving the competitiveness of a country at a particular stage of development will not necessarily be the same for a country in another stage: what presently drives productivity improvements in Japan or France is different from what drives them in Algeria or Uganda,” the report notes.

The aim of the report is to try to understand why some countries have managed to attain and maintain higher levels of prosperity than others.

It attempts to explain why countries that started off at roughly the same prosperity e.g. Botswana, Kenya, and South Korea in 1980, follow quite different economic trajectories. Kenya improved very slightly; Botswana showed a very impressive performance, increasing per capita income from 1,179 international PPP dollars in 1980 to nearly 18,000 in 2008; while Korea did even better, experiencing an 11-fold increase in its real per capita income over the period.

“The answer lies in the extent to which they have been able to put in place the enabling factors for rising productivity and the associated economic growth and sound governance in resource-dependent countries,” the report notes.