The Independent Uganda: You get the Truth we Pay the Price

The Independent Uganda: You get the Truth we Pay the Price

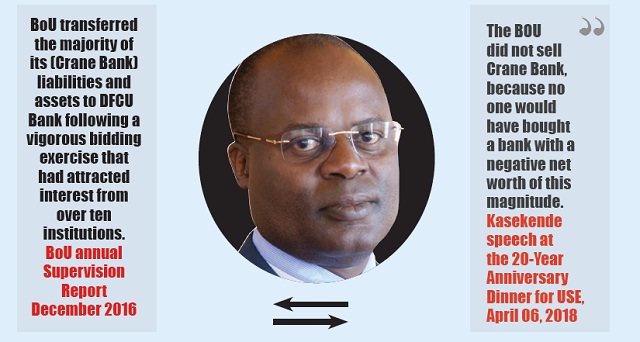

The same lawyers had advised Sudhir and DFCU. The audit firms at the centre of the deal have also been accused of conflict of interest—they audited Crane Bank when it was owned by Sudhir, severally gave it a clean bill of health but later they audited it on behalf of BoU and this time found problems with it. One of the audit firms is now one of the DFCU auditors.

BoU officials like Justine Bagyenda, have been accused of being too close to Timothy MasembeKanyerezi of MMAKS, who at one point represented Sudhir and then BoU.

Away from Crane Bank issues, the AG raises concerns about a host of other things that have gone wrong in the liquidation of the seven banks.

The AG was in a Nov.28 letter directed by COSASE to undertake a special audit on the closure of commercial banks by Bank of Uganda.

The committee specifically requested the AG to look into; the status of the banks at closure, cost of liquidation, assets and liabilities of the said banks at closure and current status, non-performing assets, non-recoverable assets and liquidators.

In a January 30 letter, the AG requested for documentation relating to all closed banks’ assets and liabilities taken over by BoU. However, the AG was not availed with documentation relating to Crane, NBC and Teefe banks.

Apparently, BoU management explained that there were pending cases challenging the closure of NBC and Crane banks and therefore an audit on how the defunct banks were closed would offend the rule of subjudice.

“Because of this limitation of scope,” the AG noted, “I could not assess the status of the assets and liabilities of these three closed banks.”

The AG notes that BOU is responsible for the preparation of the statement of affairs of the liquidated bank in accordance with FIS 1993. It is also responsible for ensuring that the bank keeps proper accounting records that disclose, with reasonable assurance, the state of affairs of the bank and safe guarding the assets of the bank.

However, the AG was not provided with all statements of affairs. Even some of the statements of affairs prepared by BOU had comparatives figures from prior years, which were not supported with the corresponding statements of affairs.

“Because of this limitation of scope,” the AG notes, “it was difficult to trace the movement in assets and liabilities from closure to date.”

Under the law, BoU is obliged to maintain inventory reports at takeover. As soon as possible, after taking possession of a financial institution, BoU is supposed to make an inventory of the assets of that institution and transmit a copy of it to the Minister.

In letters dated 30th January 2018 and 20th February 2018, the AG notes, “I requested for the inventory reports to enable me establish whether proper inventory was undertaken.”

“The inventory reports for Greenland and Co-operative banks were provided but lacked detailed schedules of loans and deposits,” the AG notes, “The inventory report for ICB was not provided. Under the circumstances, I could not confirm whether proper inventory of assets and liabilities at closure was undertaken in line with the FIS 1993.”

According to the AG, the statements of affairs for the three banks show that at closure the banks had assets worth Shs.117.7bn comprising cash, loans, property and equipment, equity investment, amounts due from related parties and balances due from other banks.

According to management, some of the assets were sold and the proceeds used to settle liabilities.

As at 30th June 2016, the asset position had reduced to Shs.19.7bn representing cash held on the recovery account.