The Independent Uganda: You get the Truth we Pay the Price

The Independent Uganda: You get the Truth we Pay the Price

Muhumuza argued that Uganda’s economy has been growing below her potential. What is it in “Uganda’s potential” that would generate growth rates higher than those experienced? Uganda is landlocked, was engulfed in civil war from 1986 to 2005 i.e. 20 out of 28 years of this growth marathon. It is neighbouring Rwanda to the south, which was engulfed in a civil war from 1990 to 2001.

To the West is Congo which has been in civil war since 1996. To the north is Sudan, which has been at war for all this period except between 2005 and 2013. And beyond we have Burundi, Somalia and Central Africa republic all of which are at war. This is not to mention that from 1986 to 2000 most of Sub Sahara Africa was stagnating.

Even a third rate economist would tell you that Uganda’s average annual GDP growth performance of 6.92% between 1986 and 2013, in these circumstances, is a miracle. Indeed no lesser a person than former Singaporean Prime Minister, Lee Kuan Yew, said in an April 14th 1988 speech, that Uganda’s world had “collapsed” and could not be rebuilt even in 100 years. Yet it took only 14 years (1986 to 2000) for our country to rebound and reach her 1970 peak in GDP per capita. This recovery, in face of such doomsday predictions, shows how remarkable Uganda’s economic reconstruction and state reconfiguration have been.

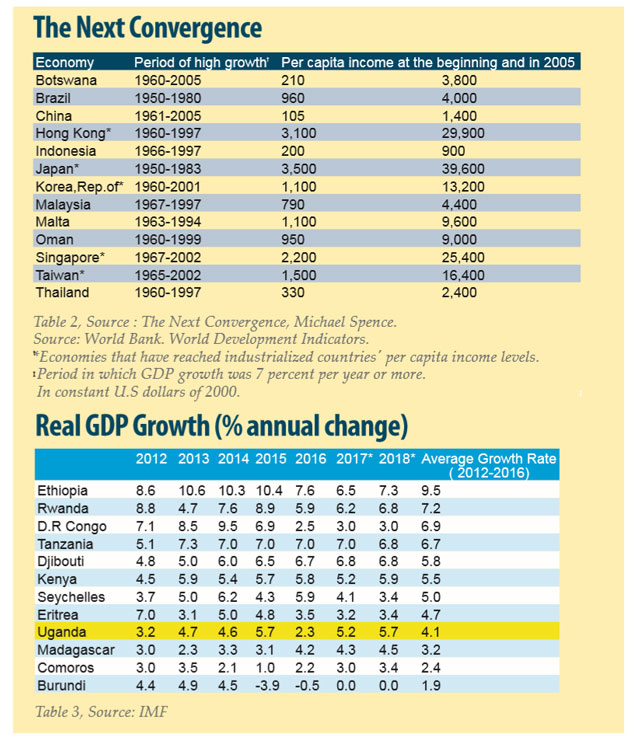

More critically for Muhumuza, historically few countries have ever sustained an average annual GDP growth rate of 6.92% for 30 years. In his book, `The Next Convergence’, Nobel Laureate in economics, Michael Spence, looked at all economies of the world from 1955 and 2005 (a period spanning 50 years). He found only 13 countries have ever sustained an annual rate of GDP growth of 7% and above over a 30 years period. I have attached Spence’s table below. No Western democracy, not even America, ever achieved this. So what gives Muhumuza confidence to declare that an annual average rate of 6.92% for Uganda over a period of 28 years is below the country’s potential?

I agree that from 2012 to 2018, Uganda’s rate of GDP growth has decelerated to 4.1%. I have attached here a table of the GDP growth rates of 12 of Uganda’s closest neighbours over this period, which shows we were number eight. So we can agree with Muhumuza that over the last seven years Uganda has performed below her potential. Why? This was a critical question that Odongotho could have brought forth. Part of the answer is embedded in the ballooning of domestic debt, which we must worry about in large part because of its high interest costs.

There are many factors. One of them is that in 2012, Uganda passed the Anti-homosexuality Act. For the first time under Museveni, this decision enjoyed broad-based support across the political and social spectrum. Western donors responded by cutting aid, yet government was not willing to cut down her spending in the face of this shock. Instead it went on the credit market to borrow to fill the gap. This was the first time government of Uganda was borrowing to fund the budget; previously it only sold treasury bonds for monetary policy objectives.

As a consequence, interest on treasury bills reach 21%. Banks smelling profit shifted a lot of their lending from the private sector to government, or increased their lending rates. This was a double edged sword: on the one hand government borrowing crowded the private sector out of the credit markets while on the other it made the little credit available to the private sector extremely expensive – in some cases hitting 30%. Companies that had borrowed at lower rates all of a sudden had to pay more than they had projected. Many began to default, others would not borrow and invest, banks became vulnerable and growth decelerated.

This shock was compounded by another factor: Uganda, like most other nations of Sub Sahara Africa, had run a growth marathon of 25 years with little investment in transport and energy infrastructure. Thus as businesses expanded, demand for transport and energy infrastructure outstripped supply. Businesses increasingly faced unreliable power, constant outages, and expensive alternatives like diesel generators not to mention bad roads to transport goods across the country. This began chocking national economic growth.

This challenge was not unique to Uganda. All our neighbours to wit Rwanda, Tanzania and Kenya faced it. All of them have since been borrowing heavily to invest in transport and energy infrastructure to fill the gap between demand and supply of these critical public goods and services.

Uganda is beginning to overcome these infrastructure bottlenecks, part of the reason growth has picked apace. In 2018, Uganda’s economic growth reached 6.1%. A 2017 Harvard study projects that between now and 2025, Uganda will be the second fastest growing economy in the world – growing at 7.2%.

This may not come to pass, but it is wrong to argue that borrowing to invest in energy and transport infrastructure is wrong policy.